January has a way of making people ambitious. New planners appear. Budget apps get downloaded. Big promises float around like confetti that never quite gets swept up. It feels productive, hopeful, and slightly overwhelming all at once. Before you rush into bold money goals in 2026, pause for a moment and grab a cup of something warm. Financial goals work best when they come from clarity, not guilt. Many people set targets while still emotionally tired from December spending. That emotional fog can lead to plans that look good on paper but collapse by February. This article is here to slow things down just enough. A calmer start now saves frustration later.

Check Your Financial Pulse Before Setting Targets

Before setting goals, take an honest snapshot of where you stand. This includes balances, recent spending, and upcoming obligations. Avoid judging the numbers. They are information, not a verdict. Data becomes useful only after emotions step aside. Think of this step like checking the weather before leaving the house. You would not plan a picnic during a storm. Financial goals deserve the same logic. Knowing your current position helps you choose realistic moves. Reality makes plans stronger, not smaller.

Stop Copying Goals That Are Not Yours

Many New Year’s goals come from social pressure. Save more. Invest faster. Pay everything off immediately. These phrases sound impressive, but ignore personal context. What works for one person may feel suffocating to another. Your income, responsibilities, and stress tolerance matter. Goals should fit your life, not impress strangers. A smaller goal you actually follow beats a flashy one you abandon. Money progress is private, not performative.

Build Systems Instead of Relying on Motivation

Motivation is unreliable. It fades after long workdays or stressful weeks. Systems keep working even when energy drops. Automatic transfers, calendar reminders, and fixed routines reduce decision fatigue. A system removes drama from money choices. You do not debate saving if it happens automatically. Quiet systems do heavy lifting in the background.

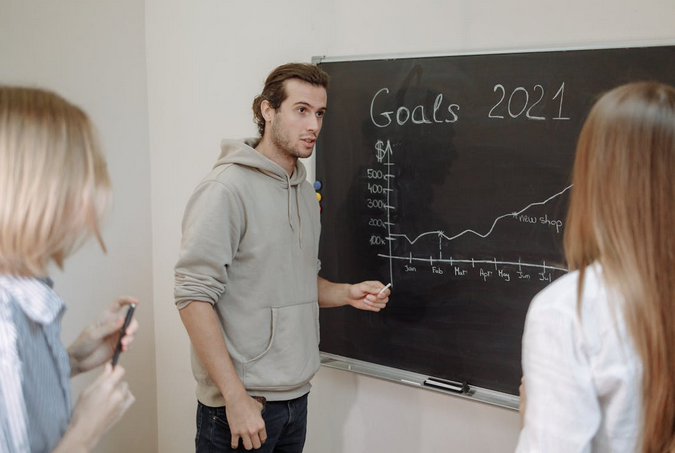

Set Fewer Goals and Make Them Boring

Ambition often shows up as a long list. Save this much. Cut that expense. Start investing. Build an emergency fund. Too many goals compete for attention and energy. That split focus usually leads to burnout. Simply pick one or two priorities. Make them simple. Boring goals tend to survive busy weeks and bad moods.

Leave Space for Flexibility and Life

Rigid goals break easily. Life interrupts plans without asking permission. Unexpected expenses, schedule changes, or emotional days happen to everyone. A good financial plan expects disruption. Build margins into your goals. Allow room to adjust without quitting. Progress does not require flawless execution. It requires resilience.

Setting New Year financial goals should feel grounding, not stressful. A slower start creates steadier results. When goals match reality, they stop feeling like chores. They become habits that quietly support your life. Take this moment to reset expectations. Choose clarity over pressure. Your future self will appreciate the patience you showed today.…

High-net-worth individuals (HNWIs) have distinct characteristics that set them apart. They often possess investable assets exceeding one million dollars, but their needs and preferences go beyond mere numbers. This group typically values personalized service and trusts firms that understand their financial goals. They seek tailored investment strategies rather than cookie-cutter solutions.

High-net-worth individuals (HNWIs) have distinct characteristics that set them apart. They often possess investable assets exceeding one million dollars, but their needs and preferences go beyond mere numbers. This group typically values personalized service and trusts firms that understand their financial goals. They seek tailored investment strategies rather than cookie-cutter solutions. Branding plays a crucial role in attracting high-net-worth clients. It creates an image of trust and reliability, essential for individuals managing significant assets. A well-defined brand communicates expertise and professionalism. High-net-worth individuals are discerning consumers. They seek personalized services that reflect their unique needs and aspirations.

Branding plays a crucial role in attracting high-net-worth clients. It creates an image of trust and reliability, essential for individuals managing significant assets. A well-defined brand communicates expertise and professionalism. High-net-worth individuals are discerning consumers. They seek personalized services that reflect their unique needs and aspirations.

One of the advantages of investing in precious metals is that they are considered a safe haven asset. When markets become volatile, investors can turn to these investments for stability and security. In addition, precious metals have an intrinsic value due to their rarity and demand, making them attractive investments even during economic downturns.

One of the advantages of investing in precious metals is that they are considered a safe haven asset. When markets become volatile, investors can turn to these investments for stability and security. In addition, precious metals have an intrinsic value due to their rarity and demand, making them attractive investments even during economic downturns.

One of the most common reasons people take out personal loans is to consolidate their credit card debt. Credit cards often come with high-interest rates and can make it challenging to pay off your monthly balance. With a personal loan, you can combine all your credit card debts into one loan with a lower interest rate, making it easier to manage your payments. This can help you save money in the long run by reducing the interest you pay on debts.

One of the most common reasons people take out personal loans is to consolidate their credit card debt. Credit cards often come with high-interest rates and can make it challenging to pay off your monthly balance. With a personal loan, you can combine all your credit card debts into one loan with a lower interest rate, making it easier to manage your payments. This can help you save money in the long run by reducing the interest you pay on debts. Finally, personal loans can also help cover unexpected expenses. For example, taking out a personal loan can provide the necessary funds to help cover an emergency expense such as an unexpected medical bill or car repair. This can save you money in the long run by allowing you to avoid high-interest credit card debt or having to dip into your emergency savings account.

Finally, personal loans can also help cover unexpected expenses. For example, taking out a personal loan can provide the necessary funds to help cover an emergency expense such as an unexpected medical bill or car repair. This can save you money in the long run by allowing you to avoid high-interest credit card debt or having to dip into your emergency savings account.

For a person thinking about the best source of income, trading may seem like a great way to earn a six figure profit yearly. There are a lot of advertisements that may lure a person to consider trading, forgetting that trading greatly depends on the market behavior. The truth is that trading can be daunting, especially for a person considering day trading as a means to earn a living.

For a person thinking about the best source of income, trading may seem like a great way to earn a six figure profit yearly. There are a lot of advertisements that may lure a person to consider trading, forgetting that trading greatly depends on the market behavior. The truth is that trading can be daunting, especially for a person considering day trading as a means to earn a living.

Buying high-quality stocks and holding them for some time is a good strategy when it comes to investing in trading. This is a good way to make sure that you make money in both the bulls and the bears market while maximizing the profits and minimizing the losses. Therefore, trading can be a good source of income, but only through the use of strategic tools and most importantly, if you know how to avoid scams. You can click here and learn more.…

Buying high-quality stocks and holding them for some time is a good strategy when it comes to investing in trading. This is a good way to make sure that you make money in both the bulls and the bears market while maximizing the profits and minimizing the losses. Therefore, trading can be a good source of income, but only through the use of strategic tools and most importantly, if you know how to avoid scams. You can click here and learn more.… make your financial future secure.

make your financial future secure. Utilizing employee benefits

Utilizing employee benefits future. That is why you have no choice but to make sure that you get the debt off your back. Fortunately, there are many things that you can do to get rid of your student’s loan burden. You can get some help from the student loan forgiveness website guide. If you are thinking about making repayment, but you want shave thousands off your student’s loan, here are the things that you can do;

future. That is why you have no choice but to make sure that you get the debt off your back. Fortunately, there are many things that you can do to get rid of your student’s loan burden. You can get some help from the student loan forgiveness website guide. If you are thinking about making repayment, but you want shave thousands off your student’s loan, here are the things that you can do; A fine is usually charged to people who do not make the required payments every month. If you want to avoid these fines, you should pay the minimum amount of money that you are required to pay every month. However, keep in mind the fact that that it will take you longer to complete the repayment of your loan if you make slow payments. Students loans attract a small interest rate every year. You will save thousands if you make an effort to complete repaying your loan within a short period.

A fine is usually charged to people who do not make the required payments every month. If you want to avoid these fines, you should pay the minimum amount of money that you are required to pay every month. However, keep in mind the fact that that it will take you longer to complete the repayment of your loan if you make slow payments. Students loans attract a small interest rate every year. You will save thousands if you make an effort to complete repaying your loan within a short period. situation where cash is required urgently. Likewise, you might have to pay your mortgage immediately or risk losing your savings due to a default in repayment. In such cases, a licensed money lender in Singapore can be beneficial.

situation where cash is required urgently. Likewise, you might have to pay your mortgage immediately or risk losing your savings due to a default in repayment. In such cases, a licensed money lender in Singapore can be beneficial. Get a loan for financial problems that banks would not consider

Get a loan for financial problems that banks would not consider